Dumb and Dumber Money

The small investor has always lost money in his own way. Now he can lose it in unison. Thank LLMs.

“Dumb money” is one of the oldest slurs in finance, and, awkwardly for the people it describes, the data has spent decades agreeing with it. In 2008 the economists Andrea Frazzini and Owen Lamont gave the insult a peer-reviewed paper. Tracking the flows of retail mutual-fund investors, they found that the stocks amateurs pile into tend to underperform for the next two years, and that by diligently reallocating their savings toward whatever felt exciting, small investors reliably made themselves poorer over time. They titled the paper, with an economist’s notion of a mic drop, “Dumb Money.” It’s a simple premise to wrap your head around: the crowd chases high-sentiment growth names at precisely the moment they are most expensive.

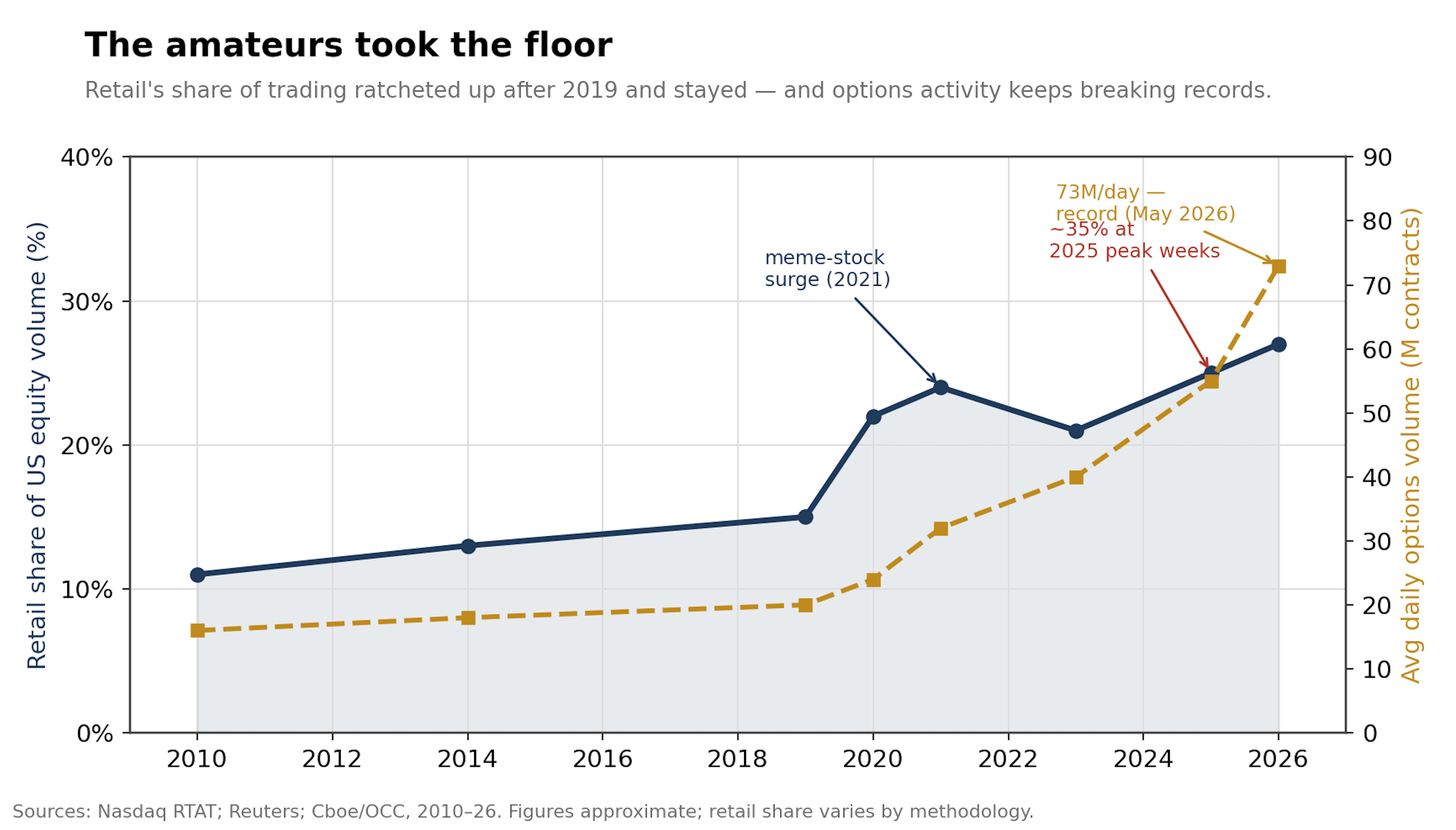

Today that crowd is larger (and louder) than at any point in living memory. Retail traders now account for something like a fifth to a quarter of daily American trading volume, spiking toward 35% in the frothiest weeks, a share that would have been actually unimaginable before commission free apps turned a brokerage account into a game. In May, average daily options volume crossed 73 million contracts, an all-time record, a great deal of it in zero day contracts that expire the same afternoon they are bought. (Yes, the SpaceX IPO belongs somewhere in this story too, but you have heard quite enough about that, and I will not bore you.)

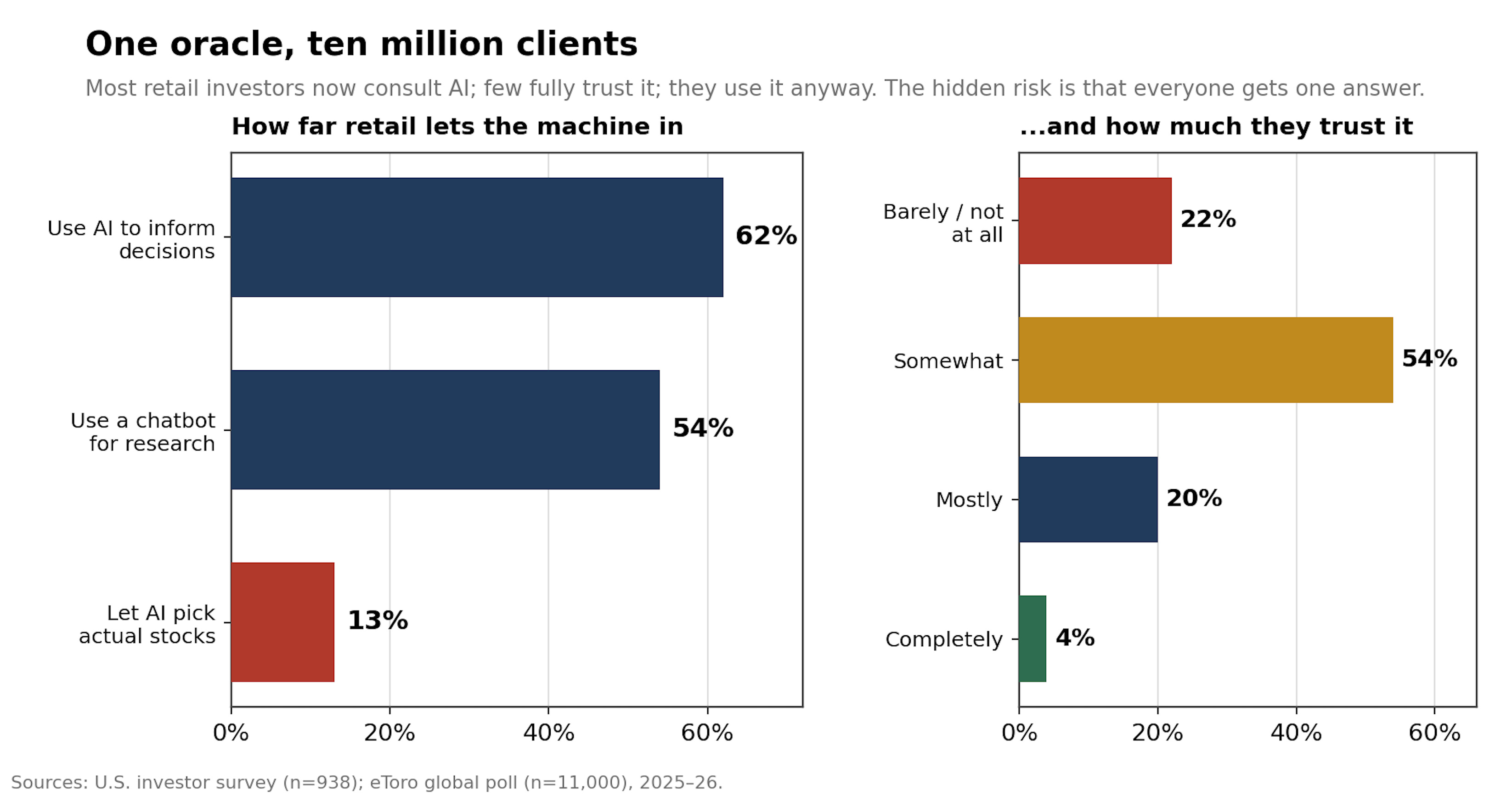

What is new is where all these people now get their ideas. In one survey of American investors, 62% said they now lean on AI tools to inform their decisions and 54% had consulted a chatbot for research; a global poll of 11,000 by the trading platform eToro found that 13% already outsource actual stock selection to ChatGPT or Gemini, with roughly half saying they would consider it. Trust, curiously, lags well behind use: most describe their faith in the machine’s advice as merely “somewhat,” only about 4% trust it completely, and close to a quarter concede they barely trust it at all, then they consult it anyway.

In Praise of Incoherence

Dumb money, historically, was actually rescued by its own incoherence. A thousand amateurs held a thousand contradictory convictions: your dentist loved gold, your cousin loved a hydrogen start-up, the man at the barbershop swore by an oil driller penny stock. Those uncorrelated errors mostly cancelled one another out. The greatest threat to this crowd crowd is the sudden disappearance of its idiosyncrasy. A large language model is a machine for manufacturing consensus. It is trained on the accumulated text of the past, so it knows best the names that are already famous. It is tuned to be agreeable, so it tends to ratify whatever enthusiasm you walk in with. And it hands the same fluent, authoritative sounding answer to everyone who types the same question. Wire ten million anxious retail investors to one sycophantic oracle and you can guess what happens next.

This is the dumb money effect, industrialized. LLMs are built to encourage what Frazzini and Lamont measured — crowding into expensive, popular, high-sentiment stocks. The tool that promised to democratize market access has unintended consequences may prove far more destructive.

Sir Isaac Buys at the Top

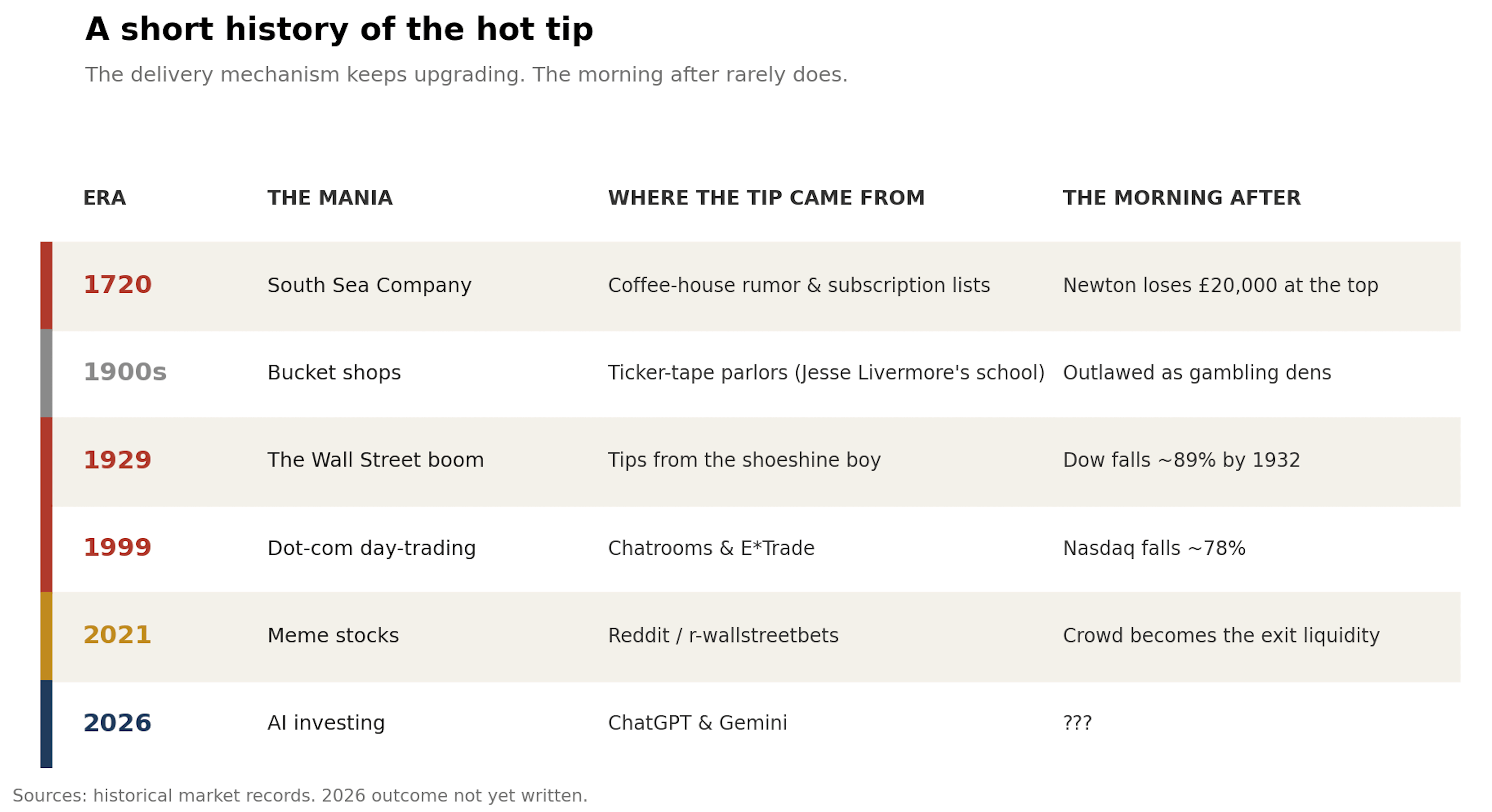

In 1720 the single most intelligent human being then alive bought into the South Sea Company, sold near the top for a hundred-percent gain of £7,000, and then, watching the price climb higher and the fortunes of lesser men balloon, bought back in close to the peak and lost £20,000, several million pounds in today’s money. Isaac Newton, who could compute the motions of the planets, was undone by the motion of a crowd, and undone specifically by re-entering after having sold like a genius. He is said to have remarked that he could calculate the movements of the heavens but not the madness of people.

Every generation relearns this with a fresh conduit for the tip. The bucket shops of the early 1900s, where a young Jesse Livermore learned the trade, were Robinhood with worse ventilation. Joseph Kennedy liked to claim he sold everything in 1929 the day a shoeshine boy offered him stock tips, reasoning that a market whose last buyer shines shoes has run clean out of buyers; the Dow proceeded to fall by roughly 89%. The day-trading chatrooms of 1999 turned Pets.com into a household joke before the Nasdaq shed nearly four-fifths of its value. The Reddit boards of 2021 discovered that a coordinated mob could briefly wound a hedge fund, then rediscovered the more durable truth that the mob is usually the exit liquidity. In each case the new tool was hailed as the great leveler, the thing that would finally hand the little guy the keys.

The chatbot is the most seductive of the list because it feels least like gambling. A tip from a shoeshine boy carries the unmistakable whiff of a tip from a shoeshine boy. A 900 word investment thesis, produced in four seconds and studded with the vocabulary of actual analysis, carries the whiff of a professional hedge fund brief. It flatters the user into mistaking fluency for edge, and because it will cheerfully agree with almost anyone, it dissolves the last bit of friction that used to slow a bad decision, which was the trouble of finding a human willing to endorse it.

Try for yourself: ask an LLM to write a 900 word buy rating stock report for any company in the entire world. Matter of fact, for the worst company in the world — one you may have been looking to short. To the eyes of “dumb money,” it’ll sound wholly convincing.

For a while, naturally, the herd will be right, which is a feature this arrangement that may be hard to grasp. If enough capital chases the same AI-anointed names, those names rise, the chatbot’s users feel vindicated, and the loop is fed again, until sentiment turns and the very synchronization that inflated the trade accelerates its collapse. Correlation is a truly marvelous thing on the way up and a stampede on the way down.

None of this means retail investors are stupid. Dumb-money isn’t always stupid. Newton was not stupid, and neither is the nurse in Ohio moving fifty dollars a week into an index fund. But dumb-money is being hit in the head by LLMs, to reproduce the one mistake they have been making since 1720 — buying what everyone else is buying, at the moment everyone else is buying it, and feeling smarter than ever while doing so. The madness of people was once a distributed system, each fool failing in his own idiosyncratic way. We have given it a central server, an LLM, and an unfailingly encouraging bedside manner. Newton, at least, had to reach his ruin one decision at a time. His descendants can now arrive at the speed of inference.

See ya, folks. And stay curious as ever!

—J&E

A very talking picture haha