One Down, Two To Go...

SpaceX has rung the bell. Anthropic and OpenAI are next. A few words on who is selling, who is buying, and why the dots only connect looking backward.

A useful discipline, when watching markets, is to attend less to what is being sold than to who is selling it, and when. The merchandise on offer this year is extraordinary, ownership in three of the most coveted private companies ever assembled, but the more instructive fact is the calendar. After the better part of five years in which almost no large company chose to go public at all, SpaceX, Anthropic, and OpenAI have each decided to do so within a few months of one another, every one of them at a price that would have read as a clerical error a decade ago. When the people who understand an asset better than anyone alive all conclude, in the same quarter, that the moment has arrived to sell a portion of it to the public, a prudent observer might pause to ask what they can see from the inside that the rest of us cannot.

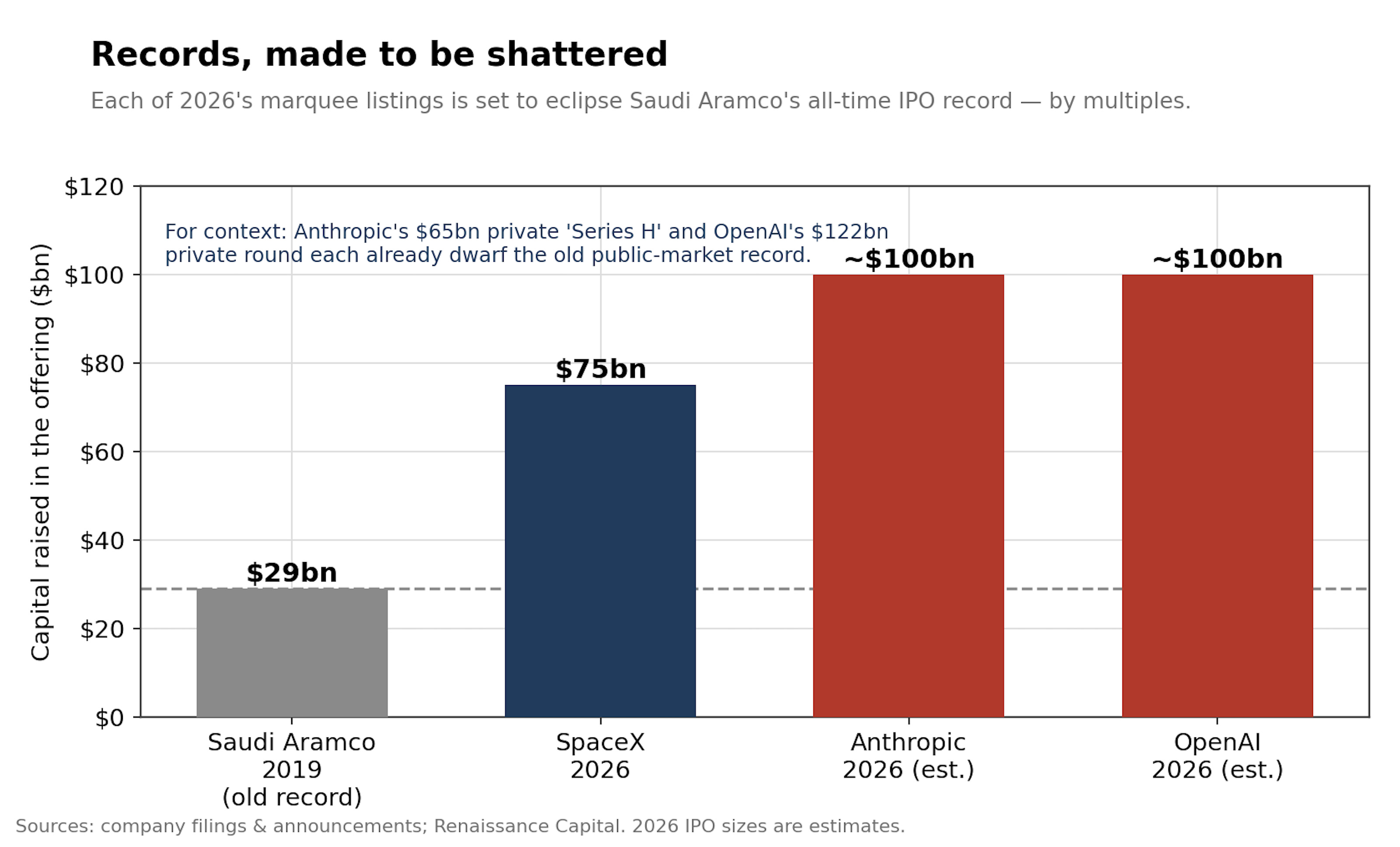

The first of the three has already gone. SpaceX has listed, raising roughly $75 billion against a valuation near $1.75 trillion — the largest initial public offering ever conducted, and close to triple the previous record, set by Saudi Aramco in 2019. Aramco at least had the courtesy to sit atop the cheapest oil on the planet; SpaceX went public at something north of a hundred times its sales, a figure that requires the buyer to underwrite a theory of the next half-century rather than a business plan. One down, two to go.

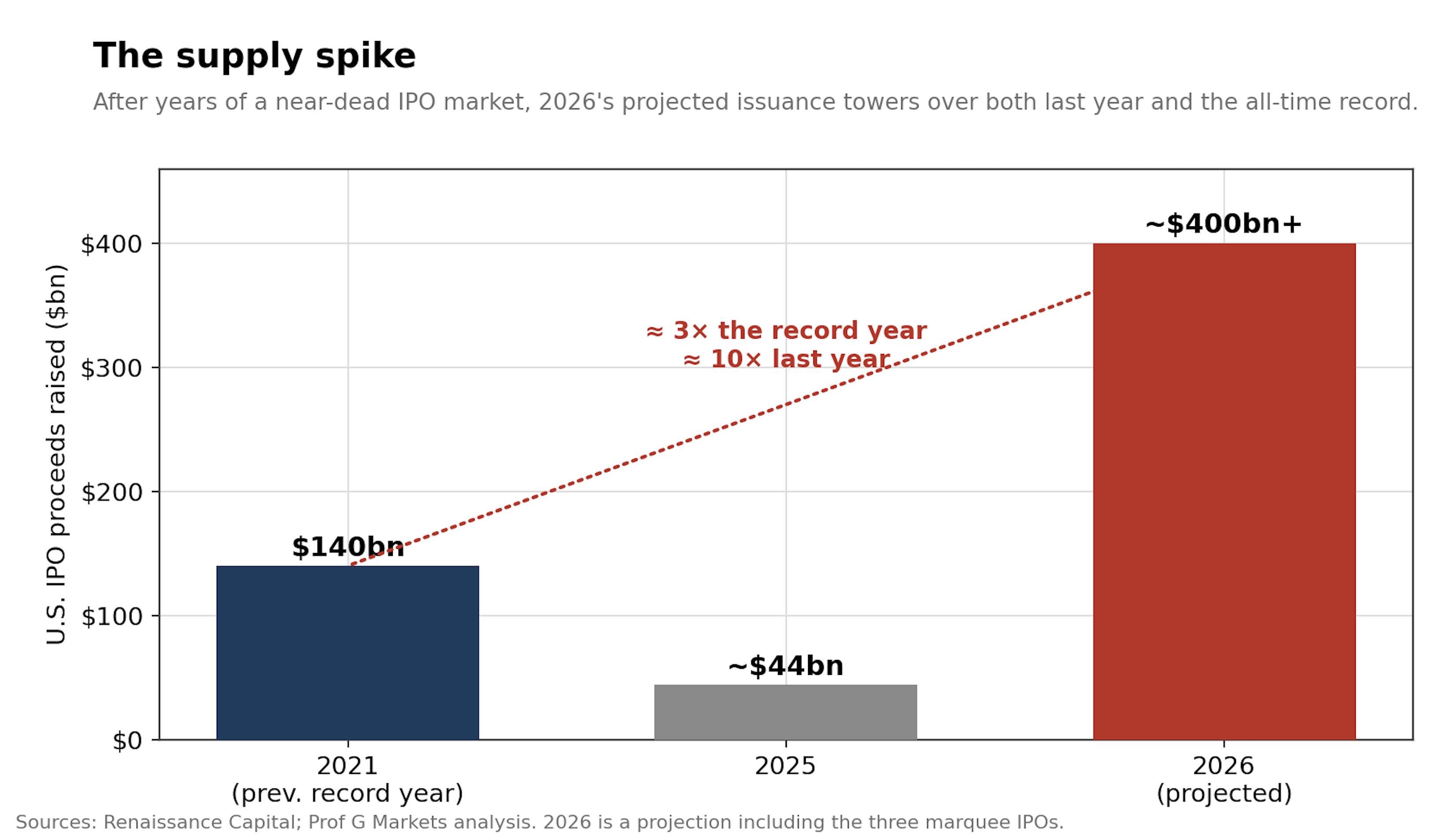

Anthropic is next. Days after closing a private round it labelled “Series H” — the eighth letter, a detail worth filing away — it submitted a confidential draft registration. Behind it stands OpenAI, whose most recent private financing reportedly valued at $122 billion, a sum that on its own exceeds the largest public offering in history by a factor of four. Assume, conservatively, that each raises somewhere around $100 billion in its debut. The three newcomers together would represent roughly $275 billion in fresh equity, enough to make this the heaviest year of new issuance ever recorded, comfortably more than double the prior peak. And that figure politely ignores the seventy-odd companies that have already floated in the months preceding them.

Keep reading with a 7-day free trial

Subscribe to Passing the Torch Newsletter to keep reading this post and get 7 days of free access to the full post archives.