The Fed Is Stimulating the Wrong Economy

Rate cuts used to create jobs. Now they fund the machines that replace them. The most powerful economic institution on Earth might be running the wrong playbook.

The Fed has a dual mandate: maximize employment and stabilize prices. For the better part of 80 years, the first half of that mandate operated on a simple premise: that cheaper capital would flow downhill into payrolls. Firms borrow, firms build, firms hire. It was elegant, intuitive, and for a long time, true. The problem with elegant models is that they tend to survive long past the conditions that made them elegant. The economy has changed underneath the Fed’s feet.

Capital is still flowing downhill. It’s just flowing into server farms and robotic arms instead of headcount.

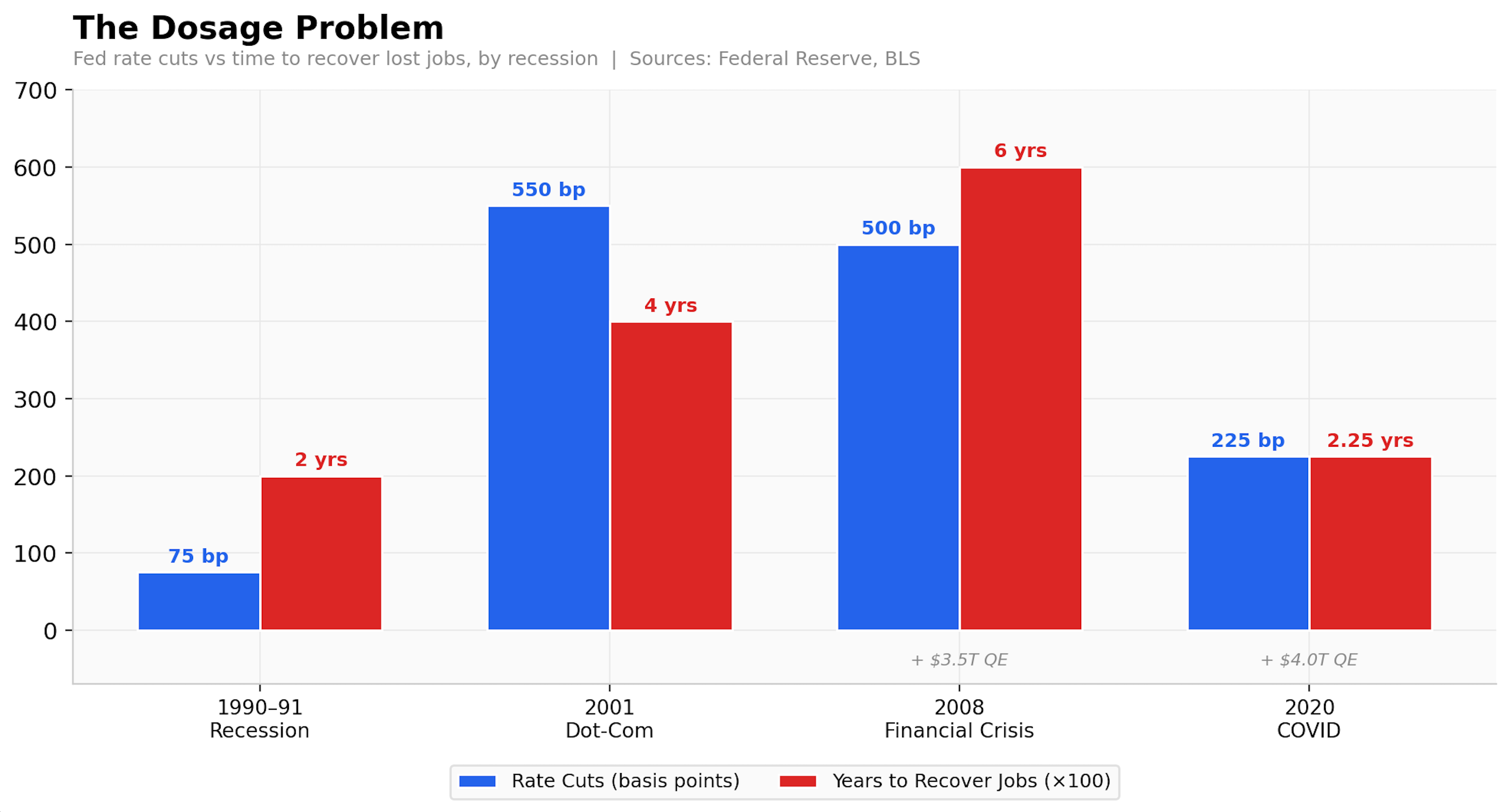

The Dosage Problem

Look at what it has taken to get the economy back on its feet after each of the last four recessions. In 1990, the Fed cut rates by 75 basis points and employment recovered within two years. In 2001, they cut 550 basis points — seven times more — and it took four years to get those jobs back. In 2008, they cut 500 basis points, launched $3.5 trillion in quantitative easing, held rates at zero for seven years, and employment still didn’t recover to pre-crisis levels until 2014. Six years.

The dosage keeps going up, and the response keeps getting weaker.

COVID complicates the comparison, but in a way that reinforces the thesis rather than undermining it. The labor market recovered in about two years (fast by modern standards) but the heavy lifting was done by $5 trillion in direct fiscal stimulus, not by monetary policy. Congress wrote checks to people. The Fed bought bonds from banks. One of those things created spending. The other created liquidity, which is a different animal entirely.

The Substitution

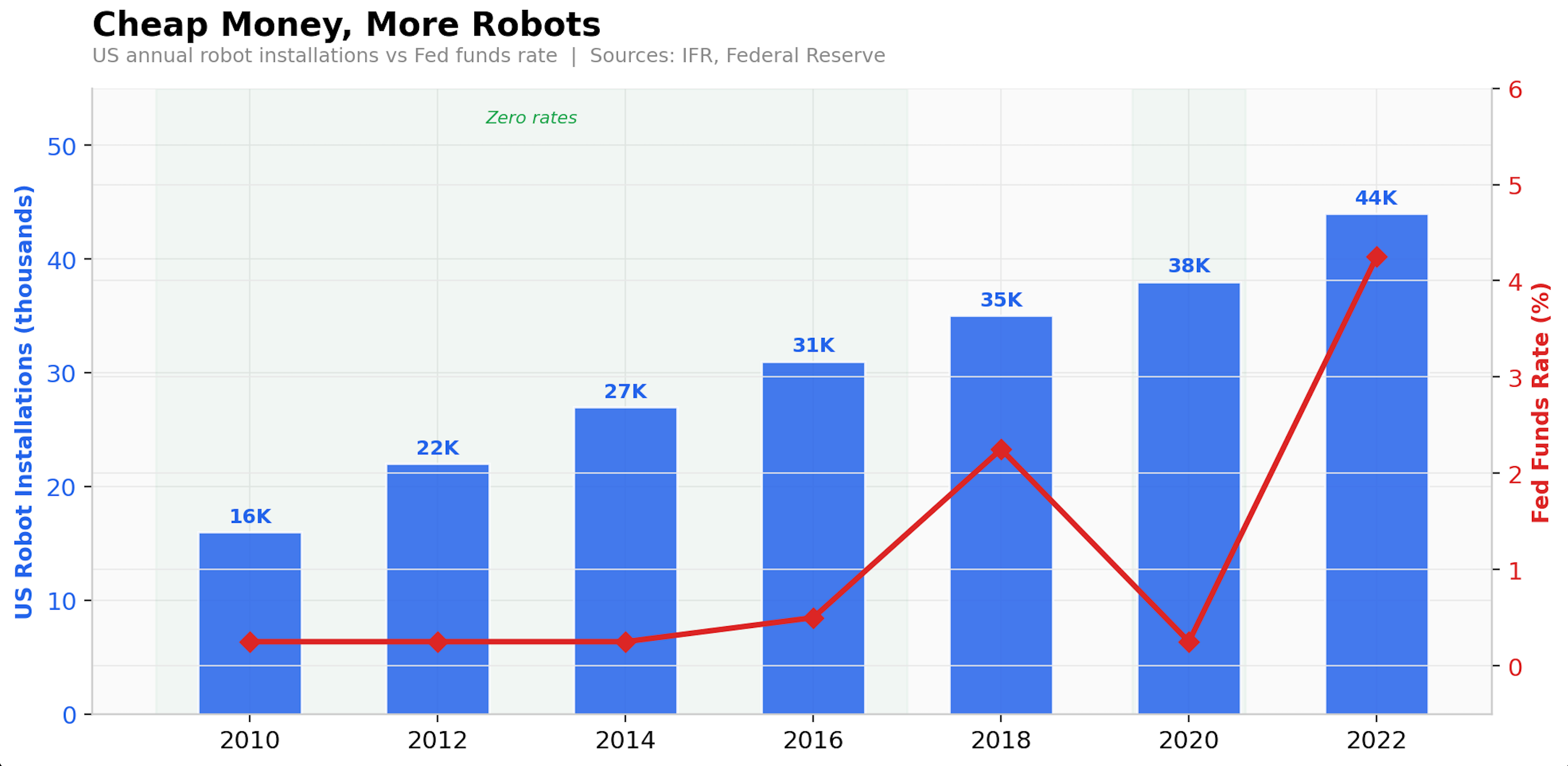

When the Fed makes capital cheap, firms face a choice: hire a person or buy a machine. For most of the 20th century, that tilted toward people. A 1960s factory robot could weld a seam. Humans were the better investment. But are they still the better investment?

Acemoglu and Restrepo at MIT found that each additional robot per 1,000 workers reduces the employment-to-population ratio by 0.2 percentage points and wages by 0.42%. When capital gets cheaper, firms substitute capital for labor. The substitution has gotten much easier now that the capital can do the work.

US robot installations went from 16,000 in 2010 — the heart of the zero-rate era — to 44,000 in 2022. Both surges in robot adoption correspond directly to periods when the Fed had rates at or near zero.

Amazon went from 1,000 warehouse robots in 2012 to 750,000 in 2023. Walmart announced that 65% of its stores would be serviced by automation by 2026. Ford and GM used cheap pandemic-era debt to build EV lines that require 30% fewer workers per vehicle than traditional assembly. This is where the cheap money went. The Fed made borrowing easy, and companies borrowed, but they just didn’t hire.

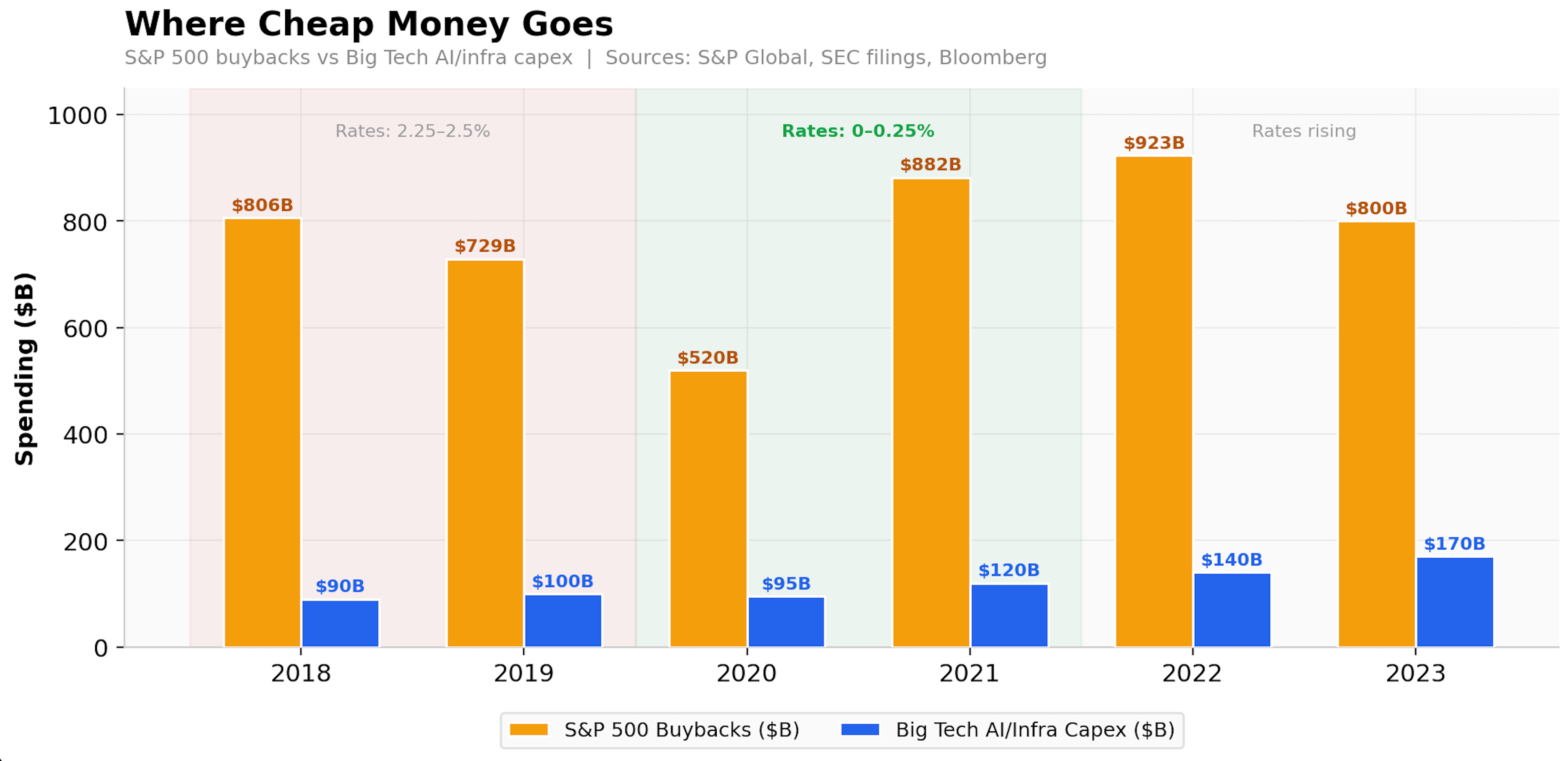

Where Cheap Money Actually Goes

S&P 500 companies spent $882 billion on stock buybacks in 2021, at the peak of the zero-rate era. $923 billion in 2022. Over six years, buybacks totaled more than $4.6 trillion. Lazonick at UMass documented the split in Harvard Business Review: S&P 500 companies spend 54% of earnings on buybacks, 37% on dividends, and only 9% on reinvestment.

The Fed’s own Boston branch confirmed it. A 2020 working paper found that firms accessing bond markets during the Fed’s corporate bond-buying program used proceeds primarily for refinancing and balance sheet management, not hiring.

So the transmission mechanism — the channel through which rate cuts are supposed to create jobs — has been rerouted. The money flows to robots, buybacks, and AI infrastructure. GDP recovers. Corporate profits recover. S&P 500 earnings hit new highs. Employment? Employment takes years. And increasingly, when those jobs do come back, they come back in different sectors, at different wage levels, in different zip codes.

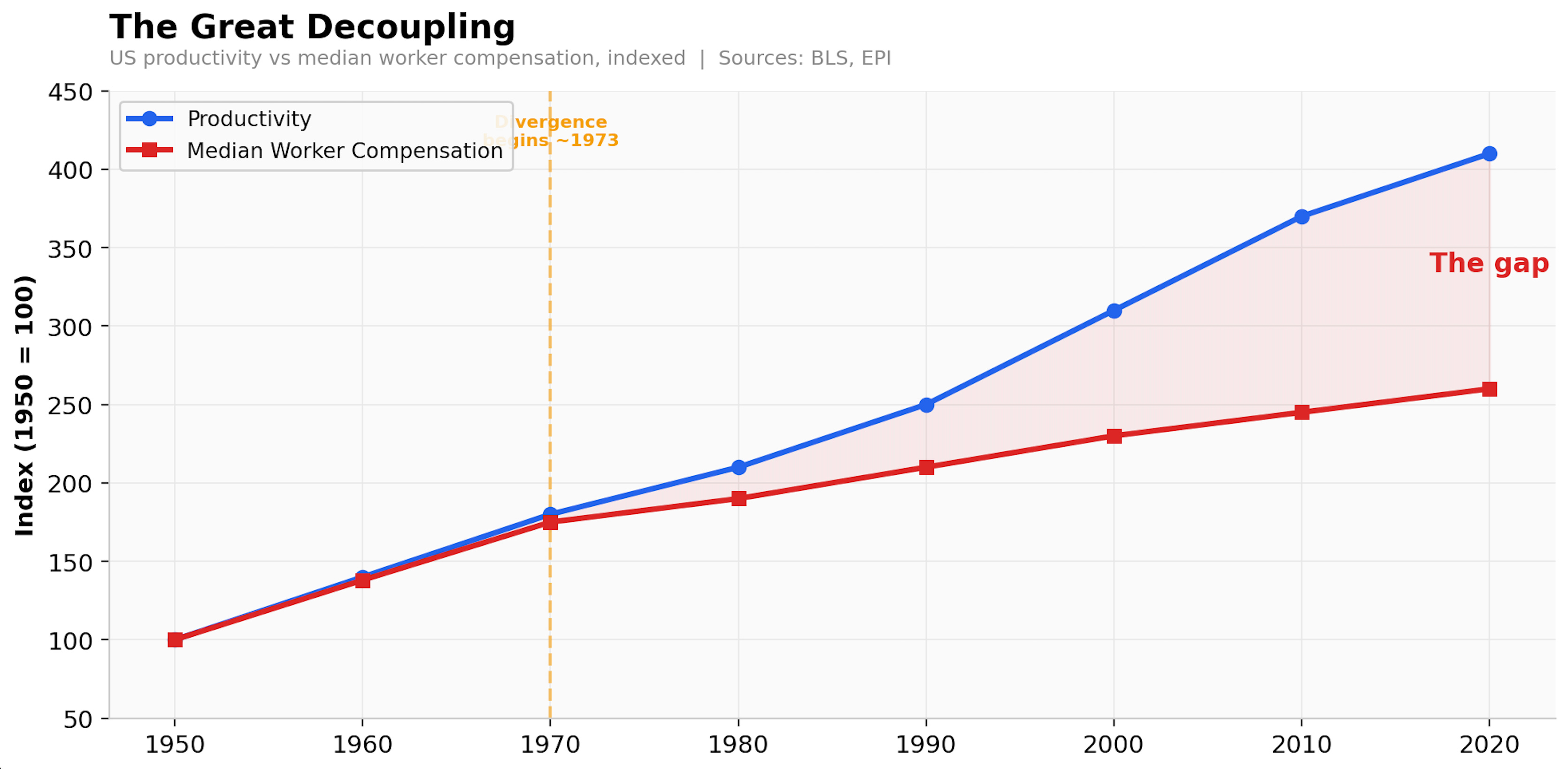

The Decoupling

From 1948 to 1973, productivity and worker compensation grew in lockstep — both roughly doubled. Since 1973, productivity has climbed another 160% while median worker compensation has grown about 17%. The Economic Policy Institute calls this the Great Decoupling, and it predates the AI boom by half a century.

The old assumption was: stimulate the economy → grow GDP → workers benefit. But the labor share of GDP has fallen from 65% to 60% since 2000. Even when monetary policy successfully stimulates growth, a shrinking slice of that growth flows to workers as wages. The Fed can make the pie bigger, but it can’t control who gets to eat.

Larry Summers calls it “secular stagnation.” El-Erian calls rate cuts “increasingly blunt instruments.” Lael Brainard, before becoming NEC Director, acknowledged in a 2019 speech that “the sensitivity of economic activity to interest rates may have diminished.” Even the people running the machine are starting to admit it might be broken.

Politics Suppress The Root of the Problem

This creates a political problem that lives in the blind spot between both parties. Trump berates Powell for not cutting fast enough; cheaper money means more growth means more jobs, or so the logic goes. Warren berates him for hiking too aggressively; tight money hurts working families first. The disagreement is front-page. The shared assumption underneath it is quiet, and more dangerous: that the Fed’s tools still transmit to the labor market the way they did when these arguments were first formulated.

There is a version of this where they don’t.

If rate cuts now primarily fund automation and financial engineering, then the Fed isn’t merely ineffective — it is actively subsidizing the displacement of the workers its mandate instructs it to protect. Each cut lowers the cost of the capital that competes with labor. Goldman Sachs estimates generative AI could automate 25–50% of the workload across two-thirds of US occupations. McKinsey projects 30% of hours worked could be automated by 2030. These estimates keep getting revised upward, and every one of them is powered by the same cheap capital the Fed provides. The dual mandate asks the Fed to maximize employment. The transmission mechanism it relies on may now be optimized to minimize it.

I don’t think the Fed is obsolete. I think it is operating with a mental model that calcified somewhere around 1998 and nobody has had the institutional courage to update it. Rate cuts still move housing, auto loans, consumer credit — the demand side is real. But the supply-side assumption — that cheaper borrowing creates proportional job growth — isn’t a good one. AI is not going to bend that curve back. AI is going to break it.

The Phillips Curve has flattened into something closer to a straight line. The jobless recovery has become the default, not the exception. The labor share of GDP declines a little more each cycle. And the most powerful economic institution on Earth continues pulling the same lever, calibrated to an economy that no longer exists, while the actual economy rewires itself underneath.

Someone should probably bring this up at the next FOMC meeting. Though I suspect they already know, which might be worse.

See ya, folks. Stay curious.

—J&E

Here is how Warsh's Fed could differ from Powell's:

https://arkominaresearch.substack.com/p/powells-last-meeting-warshs-fed-lower