The Memory Tax

A forgotten commodity chip is quietly taxing every gadget you buy: the clearest sign of who really holds power in the AI economy.

For most of this century, Apple was the company suppliers dreaded. It bought in volumes nobody else could match, and it used that heft to dictate terms, shave pennies, and leave its vendors grateful for the privilege of thin margins. So there was something almost vertiginous about the past few weeks. Apple raised the price of Macs and iPads by as much as $300, gestured at the soaring cost of memory chips as the culprit, and then watched a Micron executive named Sumit Sadana do the unusual thing of gesturing back. Apple, he suggested, had spent years paying rock-bottom prices during the industry’s slumps, starving memory makers of the profit they needed to expand, and now everyone was living with the consequences. The supplier scolded the customer, in public, and the customer had no reply.

To understand why it matters, you have to remember what memory used to be. DRAM and its cousins were the cursed commodity of technology — capital-devouring, viciously cyclical, and produced by a tight oligopoly of three firms (Micron, SK Hynix, and Samsung) that together hold north of 95% of the DRAM market and spent every cycle flooding one another into losses. The iron law of the business was that the buyer held the whip. Apple, Dell, and the rest could play the three suppliers against each other and pay accordingly. Artificial intelligence repealed that law in roughly eighteen months. Once a single class of buyer emerged — Nvidia and the hyperscalers it serves — willing to absorb the entire wafer supply at almost any price, the memory makers no longer had to court anyone. They could simply fire their old customers’ leverage.

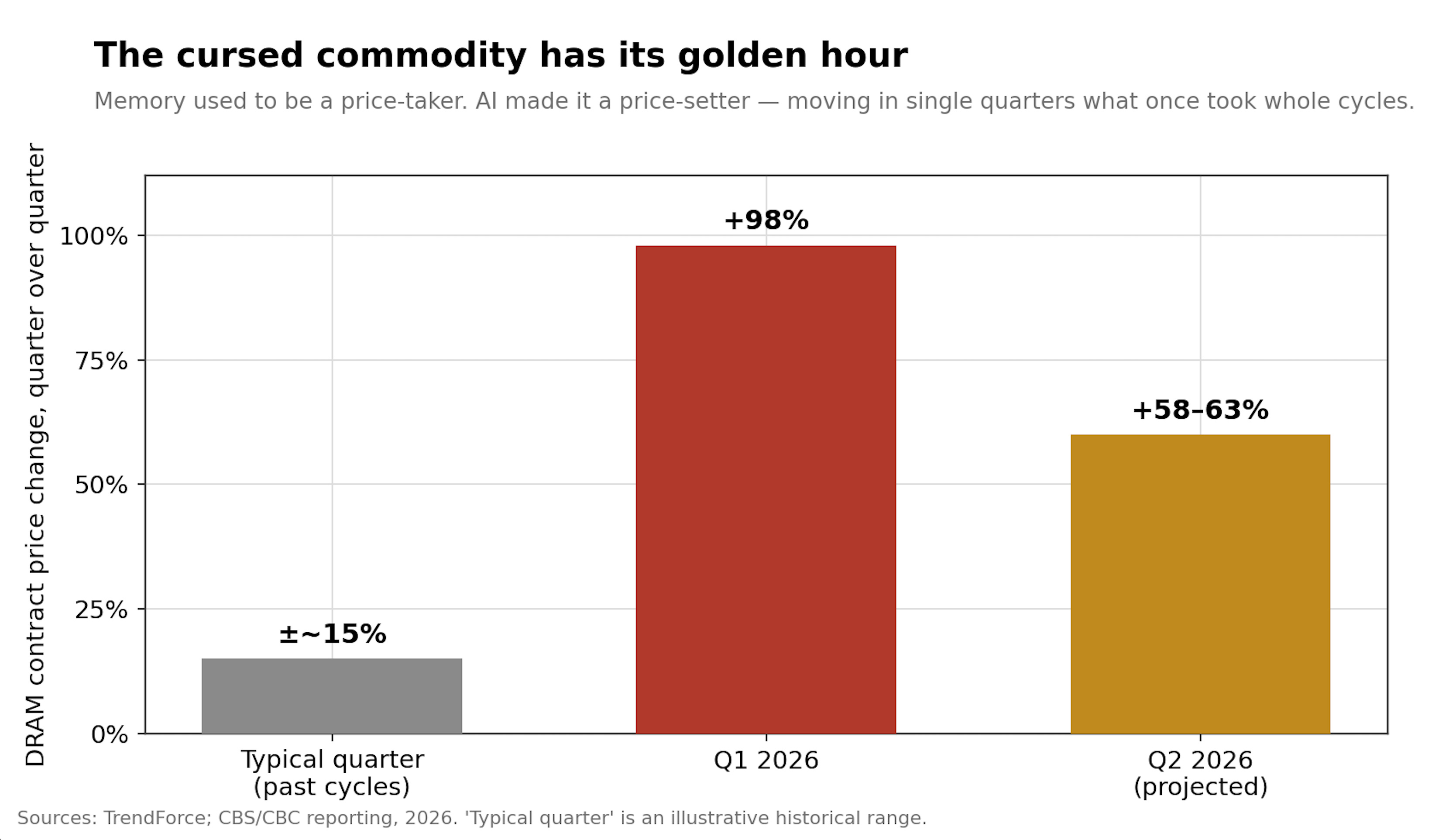

The numbers from this run-up read like a misprint. Contract prices for DRAM jumped as much as 98% in the first quarter of 2026, with forecasters at TrendForce penciling in another 58 to 63% on top of that. Micron just posted the richest quarter in its history, with gross margins it had never come close to in any prior boom.

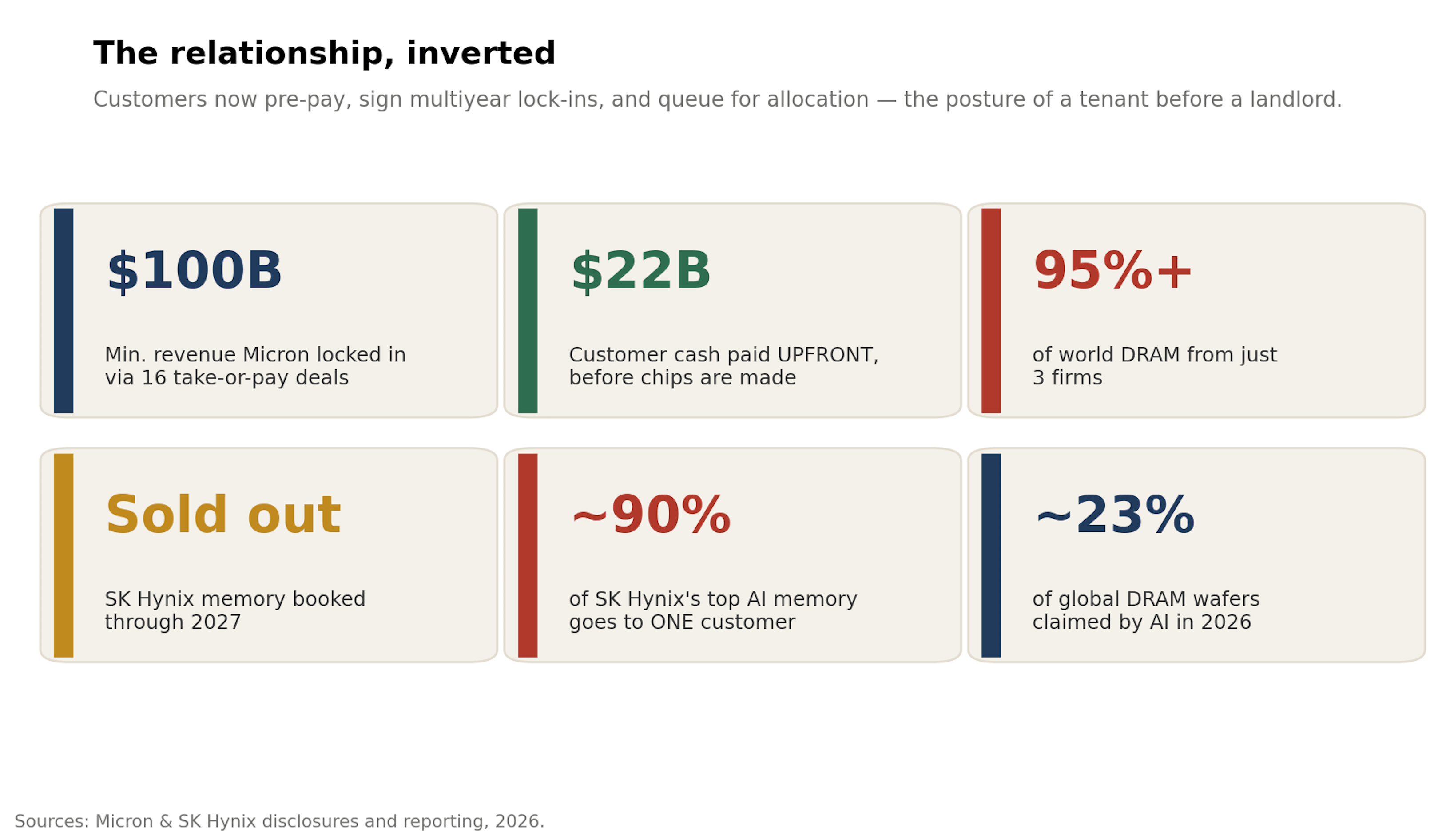

Micron used this moment to sign sixteen “take-or-pay” agreements that lock in roughly $100 billion of minimum contracted revenue and pull forward some $22 billion of customer cash, paid upfront, before the chips are even made. SK Hynix has sold out its memory production into 2027 and ships close to 90% of its premier AI memory to a single customer. Read those terms slowly. Buyers are now pre-funding the factories and signing contracts engineered to guarantee the supplier’s profit through the next downturn before the downturn has the courtesy to arrive. In the capitalism we teach undergraduates, suppliers compete for customers. Here the customers queue, leave a deposit, and plead for an allocation. That is the posture of a tenant before a landlord, or a vassal before a lord.

The bill, naturally, lands on you. AI infrastructure now consumes close to a quarter of the world’s DRAM wafer output, and the leftovers no longer stretch to cover the phones and laptops that once had first claim on them. The cost of memory inside a consumer gadget has become a levy — an AI memory tax — collected from households and remitted to data centers. Decades in which electronics grew cheaper every year have gone into reverse, and the mechanism is a transfer of real income from ordinary buyers to the capital expenditure budgets of a few enormous companies. For thirty years, the steady cheapening of computing was one of the few economic promises that reliably kept itself: a dollar bought more transistors every year, and the windfall flowed to anyone who owned a device. That promise has been interrupted by a buyer with deeper pockets than the entire consumer class combined. The household upgrading a laptop and the trillion-dollar firm wiring a data center are now bidding for the same finite slab of silicon, and the household loses every auction. It is, in the technical sense, regressive, and it is the kind of thing that stays invisible right up until a politician discovers it makes a useful villain.

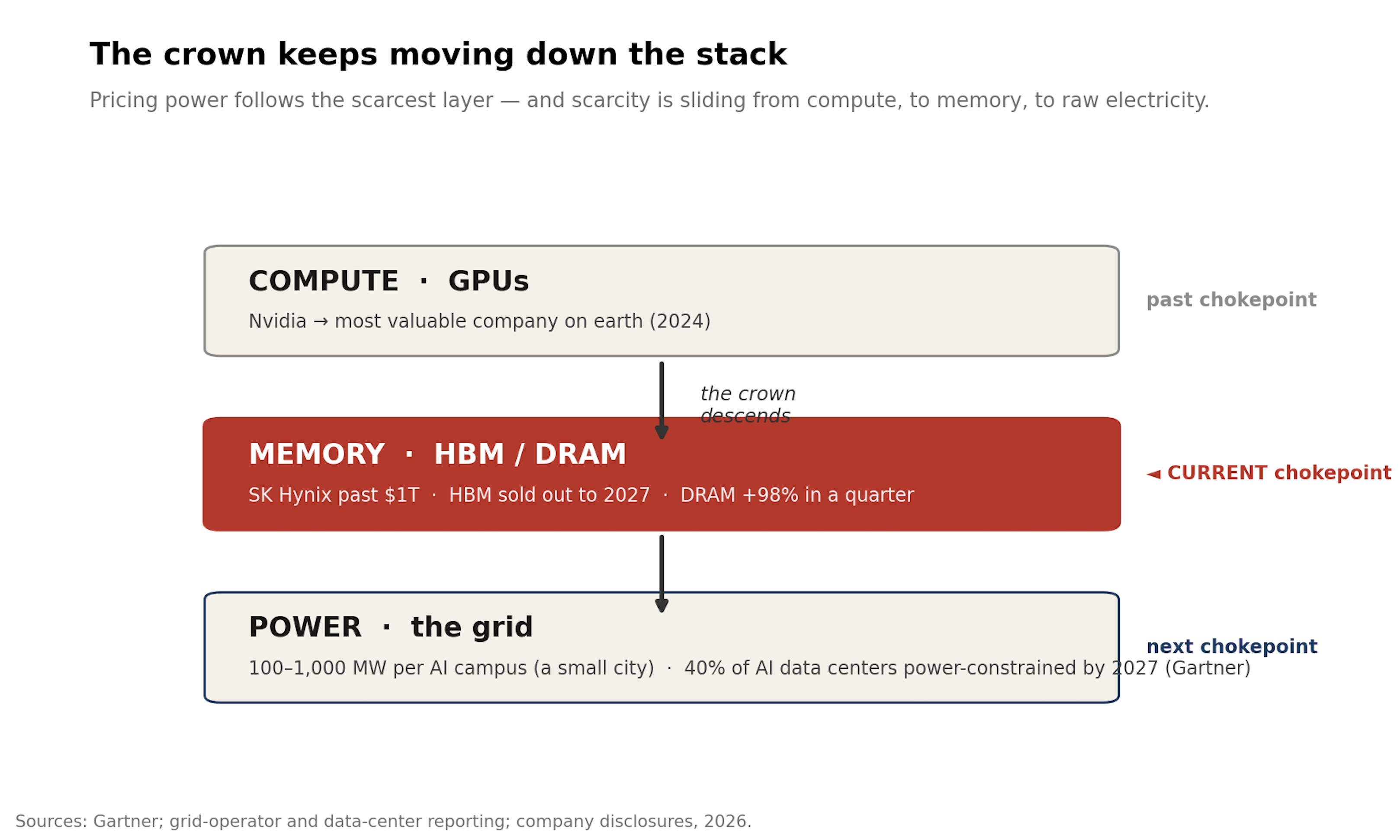

All of which raises the question the headlines keep missing: who wears the crown next? Power in the AI stack belongs to whoever controls the narrowest chokepoint, and that chokepoint has a habit of sliding downward through the layers. Eighteen months ago the scarce thing was the GPU, and Nvidia became the most valuable company on earth. Then scarcity migrated to memory, and SK Hynix vaulted past a trillion dollars in market value while Micron printed records. The next bottleneck is already visible, and it is the least glamorous input imaginable: electricity.

A single large training campus can pull between 100 and 1,000 megawatts, which is to say the appetite of a small city, and Gartner expects power shortages to throttle 40% of AI data centers by 2027. Interconnection queues now run for years; a high-voltage transformer can take longer to procure than the building it will eventually feed. The crown is descending from silicon toward copper, gas turbines, and the grid. The cloud, that most weightless of marketing words, turns out to rest on coal smoke, poured concrete, and high-voltage steel, and the people who will own the next phase of this boom are the ones who can conjure a gigawatt.

You can already see the same logic minting aristocrats elsewhere in the stack. Oracle, a database company that much of Silicon Valley had filed under “legacy,” reinvented itself as the landlord of AI compute and watched its backlog of contracted future revenue swell 363% to $638 billion — a figure now roughly three-quarters larger than the comparable backlog at Amazon Web Services. The cloud’s new nobility signs decade-long leases.

A note of caution belongs here, because memory remains memory. The same three firms have, in every previous cycle, eventually broken the truce, over-built, and detonated the price. The take-or-pay contracts are a wager that discipline holds this time, and history has not been kind to such wagers. The demand is also dangerously concentrated; when 90% of your finest product flows to one customer’s building spree, your kingdom lasts precisely as long as his capital budget. The throne is occupied, yet it is also rented, and the lease is written in AI spending that a single ugly quarter could shred.

Still, the deeper lesson is an old one, and the Gilded Age taught it first. John D. Rockefeller never struck oil; he took the refineries and the pipelines, the narrow passage every barrel had to cross. The fortunes in any boom collect wherever the system narrows to a single passage, and that passage always moves. Today it runs straight through memory, which is why a humble commodity chip now quietly sets the price of your next laptop. The crown has already begun sliding toward the power plant — and the smart money is following the scarcity down the stack, one unglamorous layer at a time.

See ya, folks. And stay curious!

—J&E

Apple raising a MacBook by $300 because a data centre in Iowa needs the same memory chip is the clearest illustration of how AI costs reach the person who never asked for AI. The consumer didn't sign up for a trillion-dollar infrastructure buildout. But the $300 on the sticker is their contribution to it, collected at the register and remitted to Micron's record-margin quarter through a commodity chip they've never thought about. For thirty years, electronics got cheaper every year. That promise just reversed, and the mechanism is a transfer of purchasing power from every household buying a laptop to the five companies buying every wafer.

The regressive part is what will eventually make this political. $300 is a rounding error for a tech worker earning $300K. It's a month of groceries for a family earning $45K. Both pay the same tax. The family can't opt out because the laptop without the price increase doesn't exist anymore. When someone in Washington figures out that the most tangible consumer impact of the AI boom isn't job loss or deepfakes but a $300 laptop surcharge funding someone else's data centre, the regulatory conversation changes overnight. Rockefeller's refineries were invisible to most Americans too, until a politician made them visible, and the memory oligopoly at 95% market share is a smaller cartel than Standard Oil ever was.

I agree that the truce is not likely to hold, but I also wonder what - at these prices - are the economics of building new fabs? When the chips were getting steadily cheaper the startup cost was a huge moat. But if the existing supply is consumed and there are still buyers with open wallets, how much of that moat remains?

Just for s&g what's the cost of a data center vs the cost of a fab plant? They're both massive capex expenditures and both have multi-year payoff horizons so it's not like just anyone can jump in. But given the hundreds of billions already pouring into capex would it make business sense to divert some of that?